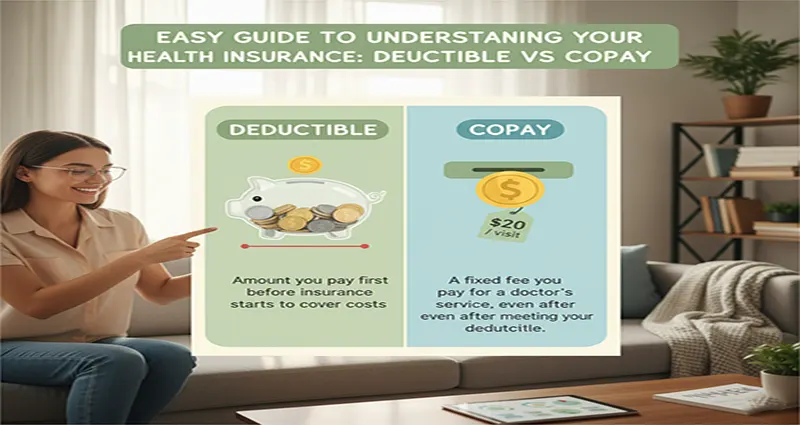

Trying to understand health insurance terms can feel like reading a foreign language. Two of the most common and important terms that determine your out-of-pocket costs are the Deductible and the Copay.

While both are ways you share the cost of healthcare with your insurance company, they work very differently and apply at different times.

1. The Deductible: Your Annual Health Care Hurdle

Think of your deductible as an annual financial hurdle you must clear before your insurance benefits fully kick in.

| Feature | Deductible |

| What It Is | A set dollar amount you must pay entirely out-of-pocket for covered medical services each year. |

| How It Works | You pay 100% of the cost for most major services (like surgery, hospital stays, or complex scans) until the total amount you’ve paid reaches this dollar amount. |

| When You Pay It | At the beginning of the year, until the full amount is met. |

| Example | If your deductible is $2,000, you pay the first $2,000 of your covered medical bills. Once you’ve paid that amount, you have “met your deductible.” |

| Resets | Every year (usually on January 1st). |

Key Point: Preventive care (like annual physicals, flu shots, and certain screenings) is usually covered 100% by your plan, even before you meet your deductible.

2. The Copay: The Fixed Fee for a Service

A copay (short for copayment) is a small, fixed amount you pay for certain routine services. It is not part of a large annual hurdle, but a transactional fee.

| Feature | Copay (or Copayment) |

| What It Is | A fixed dollar amount you pay for a specific service. |

| How It Works | You pay this fee at the time of service, and your insurance pays the rest of the cost for that visit. |

| When You Pay It | Every time you receive the specific service (e.g., every time you see your primary care doctor). |

| Example | Your plan may have a $30 copay for a Primary Care Visit, a $50 copay for a Specialist, and a $10 copay for a generic prescription. |

| Resets | Applies with every visit (does not reset annually). |

Key Point: Copays are generally not subject to the deductible and are typically charged from day one, even if you haven’t met your deductible yet.

Deductible vs. Copay: The Practical Difference

The most important distinction is when you pay them and what they apply to.

| Comparison | Deductible | Copay |

| The Role | Gatekeeper to major benefits | Transactional fee for routine care |

| The Amount | Large amount (hundreds or thousands of dollars) | Small, fixed amount (e.g., $20, $50) |

| Timing | Paid until the annual limit is reached | Paid every time you use a specific service |

| Counts toward Deductible? | The charges you pay are the deductible | Usually no (check your plan!) |

The Role of Coinsurance

Once you’ve met your Deductible, your health insurance is officially “active.” That’s when a third term, Coinsurance, kicks in.

- Coinsurance is your percentage of the cost you pay for major services after the deductible is met. A common split is 80/20, meaning the insurer pays 80% and you pay 20%.

How It All Connects: A Real-World Scenario

Imagine you have a health plan with a:

- Deductible: $1,500

- Copay (PCP): $30

- Coinsurance: 20%

| Scenario | Your Cost | How it Works |

| January: Routine Doctor Visit | $30 (Copay) | You pay the small, fixed copay up front. You don’t pay the deductible. |

| March: Broken Arm & Hospital Visit (Bill: $4,000) | $1,500 + $500 | 1. You first pay the remaining $1,500 Deductible to clear the hurdle. 2. The remaining bill is $4,000 – $1,500 = $2,500. 3. You pay your 20% Coinsurance on the remaining $2,500, which is $500. |

| October: Another Doctor Visit | $30 (Copay) | You continue to pay your $30 copay. Since you already met your deductible, your Copay is often the only charge for this routine visit. |

Understanding these three terms—Deductible, Copay, and Coinsurance—is the secret to predicting your out-of-pocket costs and choosing the best plan for your expected healthcare needs.