When it comes to health insurance, it often feels like you have to choose between saving money now and being protected later. However, by strategically opting for a higher deductible, you can significantly reduce your monthly health insurance premium, making quality coverage more immediately affordable.

This strategy, typically associated with High Deductible Health Plans (HDHPs), is not a fit for everyone, but for those who are generally healthy and have a plan for unexpected costs, it can be a powerful financial tool.

Understanding the Premium-Deductible Trade-Off

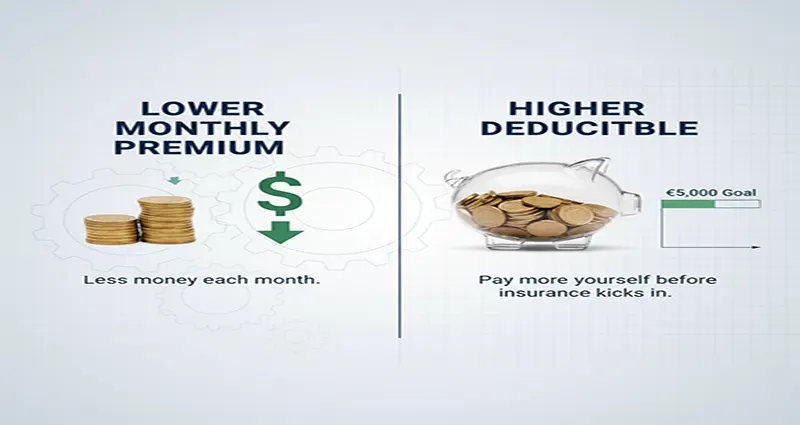

The core concept behind lowering your premium is a simple inverse relationship:

- Low Deductible High Premium: You pay more each month, but the insurance coverage kicks in sooner when you need care. This offers predictability and less financial risk in the event of a sudden illness or injury.

- High Deductible Low Premium: You pay less each month, but you are responsible for more of the initial healthcare costs (the deductible) before your insurance begins to pay its share.

By choosing the High Deductible Health Plan (HDHP), you are accepting more financial risk for medical services up front in exchange for a guaranteed, lower monthly payment.

Is an HDHP Right for You? The Ideal Candidate

A plan with a higher deductible and lower premium is typically the best fit for people who meet one or more of the following criteria:

1. The Generally Healthy Individual

If you and your family are relatively healthy and your typical medical expenses consist mainly of preventive care (annual physicals, mammograms, flu shots), an HDHP can save you significant money. Under the Affordable Care Act (ACA), most preventive services are covered at 100% even before you meet your deductible.

2. The Budget-Conscious Saver

If freeing up cash flow in your monthly budget is a top priority, the lower premium of an HDHP provides immediate and reliable savings compared to traditional plans.

3. The Prepared Saver (Crucial for Success)

This is the most important factor. An HDHP is only a smart financial move if you have, or are willing to build, an emergency savings fund specifically to cover the high deductible in case of an unexpected event. If you cannot afford to pay the full deductible out-of-pocket, the HDHP may lead to medical debt.

The HDHP Advantage: Pairing with a Health Savings Account (HSA)

The biggest financial benefit of enrolling in a qualified HDHP is the eligibility to open and contribute to a Health Savings Account (HSA). This is a powerful, triple-tax-advantaged savings vehicle that helps you manage the high deductible:

- Tax Deduction on Contributions: Money you put into your HSA is often tax-deductible or contributed pre-tax (if through an employer), lowering your taxable income.

- Tax-Free Growth: The money grows tax-free over time.

- Tax-Free Withdrawals: Withdrawals are tax-free when used for qualified medical expenses, including your deductible, co-pays, and prescriptions.

An HSA effectively turns your deductible from a looming threat into a manageable, tax-advantaged savings goal.

Pro-Tip: If your employer contributes money to your HSA, that’s essentially “free money” that lowers your effective deductible and out-of-pocket risk even further.

A Step-by-Step Strategy for HDHP Success

To maximize the premium savings of a high-deductible plan, follow this action plan:

- Calculate the Full Risk: When comparing plans, don’t just look at the monthly premium. Calculate the maximum out-of-pocket (MOOP) cost for the year. This is the absolute most you will have to pay for covered services in a year (including the deductible, copayments, and coinsurance).

- Fund Your HSA First: Make it a priority to save or contribute at least enough to your HSA to cover the full annual deductible. Treat this fund as your personal deductible safety net.

- Utilize Preventive Care: Take advantage of the 100% coverage for preventive services. Schedule your annual check-up, screenings, and vaccinations to ensure you stay ahead of any health issues.

- Become a Savvy Healthcare Shopper: Since you are paying for non-preventive services out-of-pocket until the deductible is met, you have an incentive to shop around. Use price transparency tools to compare costs for labs, imaging, and prescriptions before you get the service.

By choosing a higher deductible, you are not simply cutting corners; you are taking control of your monthly spending and strategically planning for your healthcare costs using a tax-advantaged account.